Income Tax Notice Response

Consultation for income tax notice handling and response from a Tax Expert.

- Documents Required

- TDS Certificate

- Salary Slips

- Income Tax notice

Get in Touch

Income Tax Notice

The Income Tax Department sends the notices for various reasons like not filing the income tax returns, any defect while filing the returns, or other instances where the tax department is requiring any additional documents or information.

Nothing is frightening or alarming about the notice that is received. But the taxpayer has to first understand the notice, the nature of the notice, the requestor’s order in the notice, and take steps to comply.

offers a comprehensive suite of services for families and businesses to help them in maintaining compliances. In case an income tax notice is received get in touch with the Tax Expert at to understand the income tax notice and determine a course of action.

Types of Income Tax Notice

| Type of Notice | Description |

|---|---|

| Notice u/s 143(1) – Intimation | This is one of the most commonly received income tax notices. The income tax department sends this notice seeking a response to the errors/ incorrect claims/ inconsistencies in an income tax return that was filed.If an individual wants to revise the return after receiving this notice, it must be done within 15 days.Else, the tax return will be processed after making the necessary adjustments mentioned in the 143(1) tax notice. |

| Notice u/s 142(1) – Inquiry | This notice is addressed to the assessee when the return is already filed and further details and documents are required from the assessee to complete the process.This notice can also be sent to necessitate a taxpayer to provide additional documents and information. |

| Notice u/s 139(1) – Defective Return | An income tax notice under Section 139(1) would be issued if the income tax return filed does not contain all necessary information or incorrect information. If tax notice under Section 139(1) is issued, you should rectify the defect in the return within 15 days. |

| Notice u/s 143(2) – Scrutiny | An income tax notice under Section 143(2) is issued if the tax officer was not satisfied with the documents and information that was submitted by the taxpayer.Taxpayers who receive notice under Section 142(2) have been selected for detailed scrutiny by the Income Tax department and will have to submit additional information. |

| Notice u/s 156 – Demand Notice | This type of income tax notice is issued by the Income Tax Department when any tax, interest, fine, or any other sum is owed by the taxpayer.All demand tax notice will stipulate the sum which is outstanding and due from the taxpayer. |

| Notice Under Section 245 | If the officer has reason to believe that tax has not been paid for the previous years and he wants to set off the current year’s refund against that demand, a notice u/s 245 can be issued.However, the adjustment of demand and refund could be done only if the individual has been provided proper notice and an opportunity to be heard. The recipient has to respond to the notice is 30 days from the day of receipt of the notice.If the individual does not respond within the specified timeline, the assessing officer can consider this as consent and proceed with the assessment.Therefore, it is advisable to respond to the notice at the earliest. |

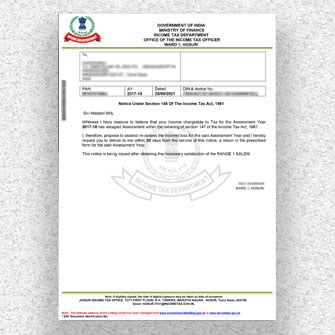

| Notice Under Section 148 | The officer may have a reason to believe that you have not disclosed your income correctly and therefore, you have paid lower taxes.Or the individual may not have filed his return at all, even if you must have filed it as per law. This is termed as income escaping assessment. Under these circumstances, the assessing officer is entitled to assess or reassess the income, according to the case. Before making such an assessment or reassessment, the assessing officer should serve a notice to the assessee asking him to furnish his return of income.The notice issued for this purpose is issued under the provisions of Section 148. |